Factoring vs. reverse factoring – what are the differences?

The service of classic factoring is used by entrepreneurs who sell goods and cannot wait for repayment from their counterparties. Their funds are frozen, and they themselves are unable to make further investments and orders because customers are dragging their feet on repayment.

Reverse factoring takes into account the situation that may arise on the other side of the transaction – so its purpose is to enable the buying entrepreneurs to pay their obligations on time, and also to assist their liquidity.

Want to know more details? Read our article where we explain the difference between classic and reverse factoring.

How to use reverse factoring?

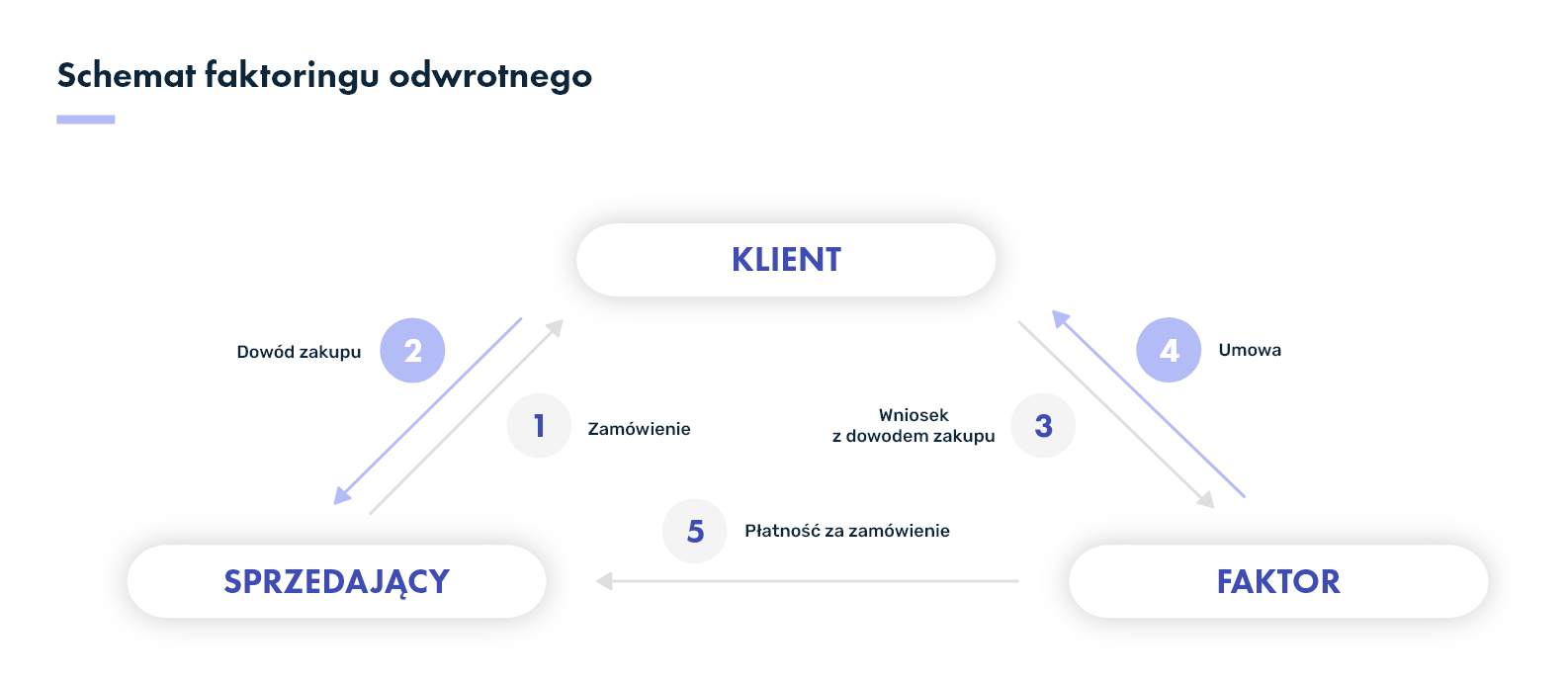

Purchase factoring is all about making it easy for an entrepreneur to finance his business purchases. To take advantage of it, you need to follow a few simple steps:

Step 1: first place an order with the seller – select the goods or services you are interested in and ask the seller for an invoice.

Step 2: once you receive it, contact the selected factor. The consultant will help you choose the most favorable solution for your company.

Step 3: apply for reverse factoring – at this stage you will present to the factor the purchase document that the seller attached to the order. This can be an invoice, proforma, order or purchase order.

Important!

Before you apply, make sure you have the required documentation. Factor requirements generally include:

- collateral with an appraisal report.

- current financial statements,

- bank statements of the established period,

- JPK_VAT files from the established period,

Step 4: after a quick verification, which should not take more than 48 hours, sign a contract with the factor.

Step 5: when you enter into a contract, the factor will immediately pay your order by express transfer, and your company will be able to settle the obligation at a later date.

Reverse factoring ensures that your company will keep the agreed payment date and will not damage its relationship with the seller or jeopardize the liquidity of its business.

The liability will still have to be repaid, of course, but with factoring you can do it in convenient installments. Their number and amount depends on individual arrangements between the factoring company and the factor.

Example:

Mr. Anatol’s company purchased a large stock of chicory directly from the importer. The seller issued an invoice with a short payment period of 7 days. The day of payment is slowly approaching, but Mr. Anatol has yet to pay three other contractors from whom he has made purchases.

Sales have been going a little worse in recent months, so the entrepreneur is not able to pay everyone on time, although he is anxious to maintain timely payment of the obligation.

In this situation, he uses a reverse factoring service – he reports the purchase invoice to his factor, the money goes into the supplier’s account the same day, and Mr. Anatol settles the payment on the date agreed with the factor.

Reverse factoring – benefits

Reverse factoring is perfect for the many situations your company may find itself in – it’s not an emergency service you resort to when things go wrong, but a beneficial solution that will help your company seize the moment, optimize your finances and take care of your liquidity. . When is it worth using it and what benefits of reverse factoring await entrepreneurs?

No negative impact on the company’s creditworthiness

Although at first glance reverse factoring may be associated with a loan, there is a powerful difference between the two: factoring is not one. This means that the use of reverse factoring will not be recorded in the BIK or other credit databases.

Banks may refuse to provide working capital or investment loans to companies that are struggling with other obligations – loans or credits. This, in turn, means that an entrepreneur who opts for reverse factoring does not thereby torpedo his company’s efforts to get credit in the future – its creditworthiness remains intact.

Image benefits

It is impossible to convert into money the benefits of paying on time and consistently building an image as a reliable business partner. And although it is incalculable, it is impossible to find any downside to this approach.

A contractor that inspires trust and actually deserves that trust is, nomen omen, a scarce commodity. So consider whether, if you have temporary problems with access to cash, it’s better to wait to pay your obligations and risk worsening your relationship with the seller, or to use reverse factoring and give your counterparty the funds it owes and your company adequate time to pay.

The use of purchase factoring does, of course, come at a cost, but incurring it to build lasting relationships with contractors can be appreciated in the future.

Deferring payments means reducing the burden on your business

Late payments – even if tolerated to some extent by your business partners – put pressure on your company. The liability, however, will not go away. Reverse factoring allows you to postpone payment of an order for up to several months. This is a period you can use to accumulate funds – for example, by recovering receivables.

Deferring payments can be especially important if your business is prone to seasonality. After all, a lack of available funds is not necessarily a symptom of your company’s financial troubles, just a worse season.

Less credit risk

Reverse factoring offers benefits not only for buyers. The seller can also benefit from it. If you sell your goods or services and your customers are other businesses, you have the option of providing long-term trade credit. However, this is a risky solution, so it is often retained only for trusted contractors.

If your company has just started working with a new contractor or you want to seriously reduce the risk, you can suggest reverse factoring to the customer. With this solution, the money will be credited to your account immediately, and the buyer will be able to make further purchases without interruption.

How is reverse factoring accounted for?

While classic factoring is quite popular (and growing), reverse factoring is not as often chosen. One reason for less interest may be fears of improper accounting for reverse factoring. How to include reverse factoring in the balance sheet?

A reverse factoring agreement is concluded between the debtor (the entrepreneur who has an obligation to pay) and the factor. As a result, the entrepreneur hands over the purchase document (or documents) to the factor, who in turn pays them. After a contractually agreed time, the debtor is obliged to pay the factor for this service – the repayment amount is increased by the factor’s remuneration (interest and/or commission).

In the accounting books, commitment factoring transactions are entered on the liabilities side of the company. In connection with the financing of obligations by the factor, the “addressee” of the obligation changes – instead of the supplier, it becomes the factor (it is the factoring company that the entrepreneur owes money from now on).

What are the costs of reverse factoring?

Depending on the entity that provides the factoring service, its costs can vary. However, any entrepreneur using reverse factoring must expect to pay interest on the financing amount – this will increase with longer repayment terms or more installments. The interest rate on factoring installments is not high, but it often depends on the amount of financing the factor decides on.

Under reverse factoring, the factor provides the entrepreneur with a factoring limit in an amount determined at the contract preparation stage. The greater the limit, the greater the amount for business purchases available to the factor. However, keep in mind that some factoring companies may charge additional fees for not using the allocated limit. At PragmaGO, maintaining your limit is free – when you choose reverse factoring, you only pay for the portion of your limit that you use.

Other fees you may encounter are:

- the commission for the transfer of receivables.

- preparation fees,

- commission for changing the terms of the contract,

Important!

Remuneration to the factoring company, such as commission or interest, is a cost of the service purchased by the entrepreneur, so it can be included as a deductible expense and reduce the income tax to be paid

Summary

Purchase factoring can help your company take advantage of an upcoming opportunity – for example, when an opportunity arises to purchase needed goods at discounted prices. It will also come in handy if your company is in a more difficult period, for example, because of the ongoing pre-season.

Remember, however, that reverse factoring is not a loan or credit. So it won’t burden your company’s credit history, but it does require collateral. Also consider the fact that with purchase factoring you can usually finance only purchases from domestic suppliers.